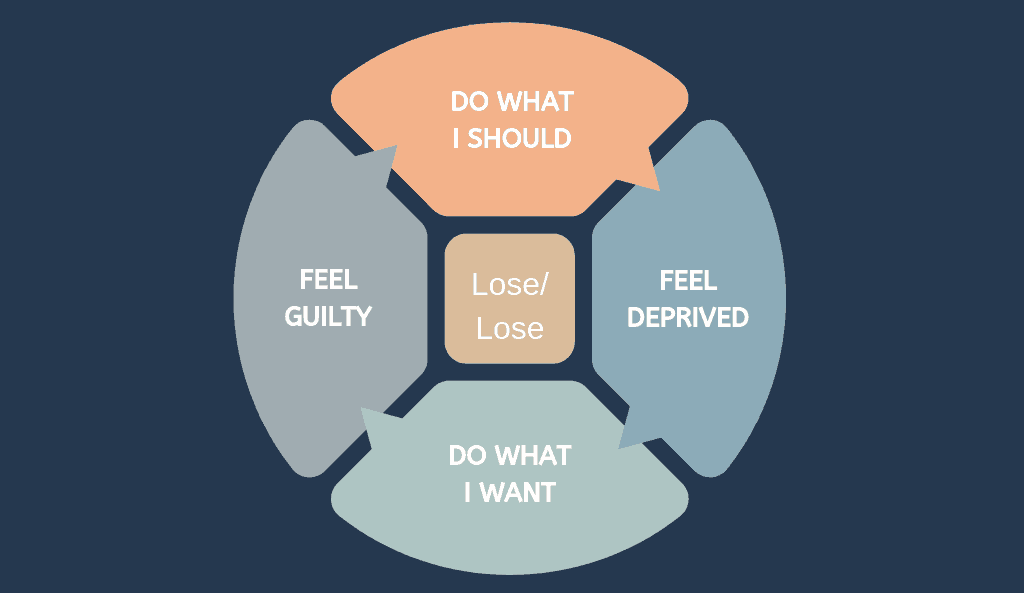

Fear, Guilt and the Spending Cycle

Spending money is rarely just about buying things. It is often about managing emotions. Fear whispers that you might miss out. Guilt reminds you that you should be saving more. Together, they can trap you in a loop that feels impossible to break. When the cycle spins long enough, people may start exploring bigger solutions like debt consolidation to regain control. But long before balances grow, the emotional pattern is already in motion.

Fear and guilt do not just appear after spending. They are often the drivers behind it.

Understanding this cycle requires looking beneath the surface of transactions. It means asking not only what you bought, but why you bought it.

How Fear Starts the Loop

Fear is powerful. It can show up as fear of missing out, fear of scarcity, or fear of not measuring up. Maybe you grew up in a household where money was tight. Maybe you experienced job loss or financial instability. Those memories leave emotional imprints.

When fear of scarcity lingers, it can create two opposite reactions. Some people hoard money aggressively. Others spend quickly, driven by a sense that resources might disappear anyway. This reaction is not irrational. It is emotional conditioning.

Behavioral economists have long studied how past experiences influence financial choices. The Consumer Financial Protection Bureau provides research on how financial well being is shaped by both objective circumstances and psychological factors. Fear tied to past instability can quietly influence present day spending.

For example, a sudden sale might trigger urgency. If I do not buy this now, I will lose the opportunity. In that moment, fear overrides long term planning.

The Temporary Relief of Emotional Spending

Spending can feel soothing. It offers control. It delivers immediate gratification. It distracts from stress or insecurity. The brain responds with a burst of dopamine, reinforcing the behavior.

After a stressful week, ordering something new or booking a spontaneous experience can feel like reclaiming power. The purchase becomes less about the item and more about the emotional shift.

However, the relief is temporary. Once the excitement fades, reality returns. The credit card balance remains. The budget tightens. And this is where guilt enters.

Guilt as the Aftermath

Guilt often follows emotional spending. You know you intended to save. You told yourself this month would be different. When you break your own plan, cognitive dissonance kicks in.

Cognitive dissonance occurs when actions conflict with beliefs. If you see yourself as financially responsible but overspend, that gap creates discomfort. The American Psychological Association explains how cognitive dissonance motivates people to resolve inconsistencies between beliefs and behaviors.

Guilt can lead to harsh self criticism. You might promise extreme restraint next month. You might swear off all discretionary spending. These rigid reactions often set the stage for the next cycle. Deprivation builds pressure. Pressure fuels another emotional purchase. And the loop continues.

Scarcity Memories and Present Behavior

Fear and guilt often have roots in past experiences. If you grew up hearing constant worry about bills, you may associate money with anxiety. If you were praised for saving but shamed for spending, enjoyment may carry emotional weight.

These early patterns shape adult habits. Without awareness, they operate automatically. You may not consciously think, I am afraid of scarcity, but your behavior reflects it.

Recognizing these patterns is not about blame. It is about clarity. When you see the connection between past experiences and current reactions, you gain choice.

Breaking the Cycle with Awareness

The first step in breaking the spending cycle is noticing it in real time. Before making a purchase, pause and ask, What am I feeling right now? Is this fear, boredom, stress, or genuine need?

Naming the emotion reduces its intensity. Instead of being swept along by impulse, you create space to decide.

Another helpful strategy is separating emotional relief from financial action. If stress is the trigger, choose a non financial coping method. Take a walk. Call a friend. Write down what is bothering you. Let the emotion settle before spending.

Building Flexible Financial Plans

Rigid budgets often intensify guilt. When every dollar is tightly controlled, small deviations feel like failure. A more sustainable approach includes room for enjoyment.

Design a plan that allocates a specific amount for discretionary spending. When purchases fall within that range, guilt has less ground to stand on. You are not breaking the rules. You are following them.

Automation also reduces emotional interference. Automatic transfers to savings remove the daily negotiation between fear and desire. When savings happen first, spending decisions become clearer.

Replacing Guilt with Accountability

Guilt tends to focus on shame. Accountability focuses on adjustment. If you overspend one month, instead of spiraling into self criticism, review what happened. What emotion was present? What situation triggered it? What can you adjust next time?

This shift from judgment to analysis builds resilience. It transforms mistakes into data rather than proof of failure.

Over time, this approach weakens the fear and guilt cycle. You become less reactive and more intentional.

Creating a Healthier Emotional Relationship with Money

Fear and guilt are not enemies. They are signals. Fear can highlight a desire for security. Guilt can signal misalignment with personal values. When interpreted constructively, both emotions can guide healthier choices.

The goal is not to eliminate emotion from spending. It is to integrate emotion with awareness. When you understand why you spend, you gain control over how you spend.

The spending cycle fueled by fear and guilt can feel overwhelming. But with mindful pauses, flexible planning, and self compassion, it becomes manageable. Over time, emotional spending loses its grip, and financial decisions start to reflect intention rather than impulse.