Choosing A Repayment Strategy That Fits Your Mindset

Repayment Is As Much Psychological As It Is Financial

When people talk about paying off debt, the conversation often centers on numbers. Interest rates, balances, payment schedules, and timelines usually dominate the discussion. While these financial details matter, there is another factor that often determines success: mindset.

Repayment strategies work best when they match how someone thinks, stays motivated, and handles long term commitments. A strategy that looks mathematically perfect on paper may fail if it does not align with the way a person actually manages habits and decisions.

For some individuals, that alignment might include exploring structured options such as a debt reduction program while reorganizing their broader financial approach. The key idea is that repayment success rarely comes from numbers alone. It often comes from choosing a method that encourages consistent follow through.

Understanding how mindset influences financial behavior can make the repayment process far more manageable.

Why Motivation Matters in Repayment

Debt repayment often takes months or even years. During that time, maintaining motivation becomes one of the biggest challenges.

Some people stay motivated by seeing quick progress. Others remain focused when they know they are minimizing interest costs. The strategy that works best depends on what type of feedback keeps someone engaged in the process.

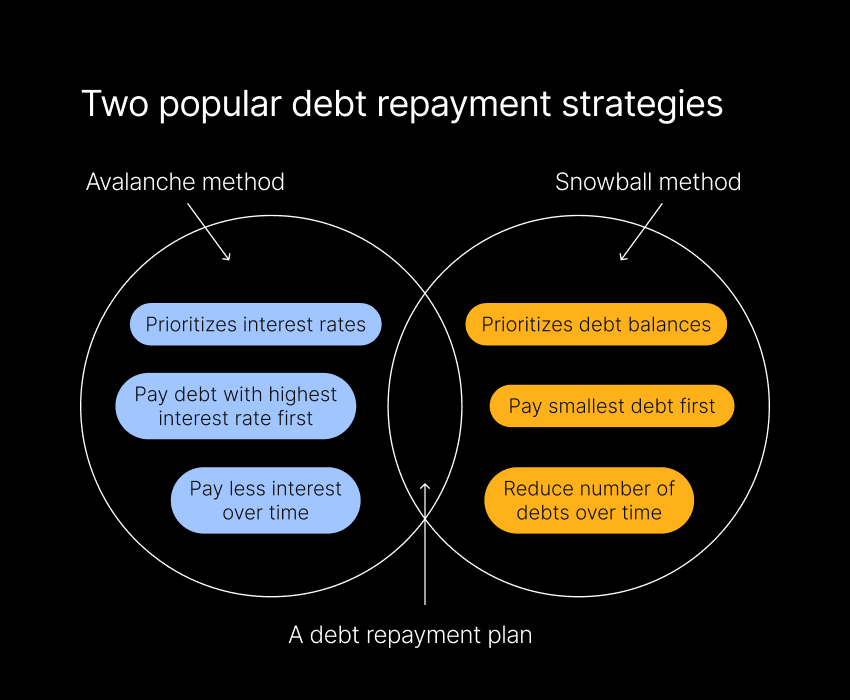

For example, individuals who prefer visible progress might respond well to strategies that eliminate smaller balances first. Each completed account creates a sense of accomplishment that encourages continued effort.

On the other hand, individuals who prefer efficiency may feel more motivated by strategies that prioritize higher interest debts first. Seeing interest costs decline can provide its own form of motivation.

Financial educators frequently highlight the role of behavioral psychology in repayment success. Research discussed by the Consumer Financial Protection Bureau guidance on debt management shows that repayment plans are most effective when they align with the habits and motivations of the person using them.

Motivation keeps repayment strategies alive long enough to succeed.

Understanding Your Financial Personality

Before choosing a repayment strategy, it can help to consider personal financial tendencies. Some people naturally enjoy detailed planning and long term calculations. Others prefer simple systems that reduce decision making.

Someone who enjoys spreadsheets and long term planning may thrive with a detailed repayment schedule that carefully optimizes interest savings. They may enjoy monitoring progress and adjusting their plan as circumstances change.

Meanwhile, someone who prefers simplicity might benefit from a straightforward system that requires fewer calculations. A clear order of payments and automatic transfers can help maintain consistency without constant analysis.

Recognizing these tendencies is not about labeling strengths or weaknesses. It simply helps individuals select strategies that match their natural approach to managing tasks.

When financial systems match personal habits, they are far more likely to be sustained over time.

Consistency Often Beats Perfection

One of the most common mistakes in repayment planning is focusing too heavily on the mathematically ideal strategy while overlooking whether the strategy can be maintained consistently.

A repayment plan that saves the most interest may still fail if it feels discouraging or complicated. In contrast, a slightly less efficient strategy that someone follows consistently often produces better real world results.

Consistency matters because debt reduction is a cumulative process. Each payment builds upon the previous one, gradually reducing balances and improving financial stability.

This perspective can reduce pressure during the repayment process. Individuals do not need a flawless strategy. They need a system that encourages steady progress.

Over time, consistent effort transforms even modest payments into meaningful improvements.

Flexibility Helps Sustain Long Term Progress

Life rarely follows a perfectly predictable financial path. Changes in income, unexpected expenses, or shifting priorities may require adjustments to a repayment strategy.

Flexibility allows individuals to adapt their approach without abandoning their overall goal.

For example, someone might temporarily reduce extra payments during a challenging financial period and then increase them again when circumstances improve. Others may shift the order of their payments if new obligations arise.

This adaptability ensures that the repayment process continues even when conditions change.

Educational materials from the Federal Trade Commission consumer credit guidance emphasize the importance of reviewing financial plans periodically and adjusting them as needed.

Repayment strategies should evolve alongside the financial realities of everyday life.

Tracking Progress Builds Confidence

Another powerful way to support repayment success is by tracking progress regularly. Seeing balances decline over time provides tangible evidence that efforts are working.

Tracking does not need to involve complex tools. Many people simply record their remaining balances each month or update a progress chart. Others prefer budgeting apps that automatically display repayment milestones.

These visual indicators reinforce motivation by showing how far someone has come rather than focusing only on how far they still need to go.

Progress tracking also helps identify opportunities to accelerate repayment when additional funds become available.

Over time, the visible reduction in debt balances can become one of the most encouraging aspects of the entire process.

Support Systems Strengthen Commitment

Debt repayment can sometimes feel isolating, especially if individuals believe they must handle the process entirely on their own. In reality, support systems often play a valuable role in maintaining motivation.

Financial counselors, educational resources, or supportive friends and family members can provide encouragement and accountability during challenging periods.

Discussing repayment goals with trusted individuals may also help reinforce commitment. Knowing that someone else understands the plan can increase the likelihood of staying on track.

Support systems transform repayment from a solitary task into a shared journey toward financial improvement.

Choosing A Strategy That Works For You

The most effective repayment strategy is not necessarily the one recommended in every financial article or calculator. Instead, it is the one that fits your mindset, habits, and long term motivation.

Some people thrive with detailed financial optimization. Others succeed with simple, straightforward systems that emphasize visible progress.

What matters most is choosing an approach that encourages consistency and confidence.

By aligning repayment strategies with personal motivations and habits, individuals create systems that support steady progress rather than temporary effort.

Over time, that alignment makes it far easier to remain committed to the ultimate goal of financial freedom.